Black- Scholes Model for Non Math Users

Call = Borrowing + Buying D of the Underlying Asset

Put = Selling Short D on Underlying Asset + Lending

To replicate the cash flows on a call option without actually buying the option, we need to borrow some money (put in some personal equity) and buy D units of underlying asset. At the end of the time period if the stock price goes up you can sell the stock and repay the borrowed amount (+ interest) and the balance is your profit. Similarly with a put option, you sell short on the underlying asset at the beginning of the period and lend the amount at an interest rate i. At the end of the time period t, if the price of the underlying asset decreases and the principal + interest you received from the borrower can be used to square of your short position and you keep the difference as your profit.

The cash flows on the option and the replication portfolio are the same and in case there is a difference there is scope for arbitrage. Arbitrageurs chip in to ensure that there is an equilibrium in these prices.

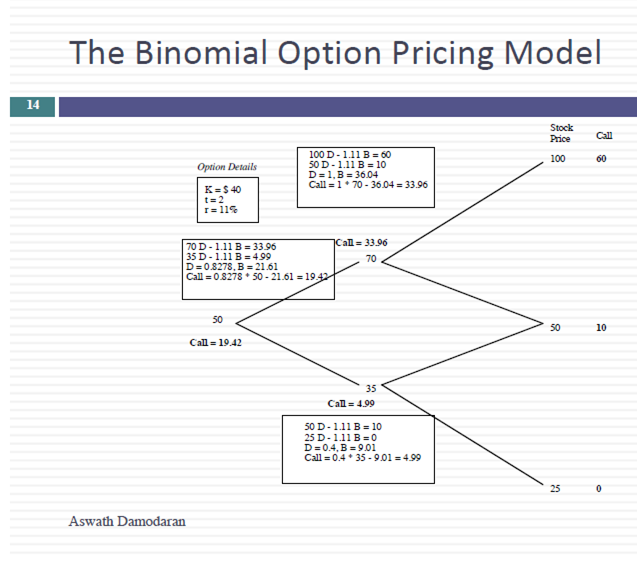

In a two period binomial model, we can easily determine the price of the options by working backwards as shown in the figure below. The number of shares that you need to buy in case of a call option is given by D, B is the borrowed amount, K is the strike price, t is the number of time periods, r is the interest rate per period.

By equating the cash flows on the replication portfolio and the call, we are implicitly assuming zero arbitrage and thus we can arrive at the price of the option today. (working backwards from the cash flows at the end of the period)

In the real world, asset prices change continuously and the Black Scholes model is just an extension of the two period model in to the real world in which asset prices change continuously and are normally distributed.

Remember those pay off diagrams for calls and puts. A call option derives value only when the underlying asset is at a price above the strike price. Similarly a put option derives its value only when the price is below the strike price of the option.

|

| Payoff on Options |

Once you have an understanding of these basic ideas it is not really difficult to use the Black Scholes model which is presented below.

|

| The Black Scholes Formula for Calls and Puts |

where

C is the price of the call option

P is the price of the put option

S is the Stock Price

K is the strike price

y is the annual dividend yield - dividend paid/current market price of the underlying stock

t is the time period

r is the interest rate per time period

? and sigma for standard deviation

When we move from a two period model to a continuously compounding model, the value of money is assumed to compound at e units per unit of time, e is the euler's number which is equal to 2.7182818284590452353602874713527 (and more ...). So in the equations above determining call and put prices where we use K*e^(-r*t), we are just determining the present value of the strike price as we do not have to forgo or receive the strike price till the end of the period.

A call derives its value only when it is in the money, that is only when K < S, so to arrive at the price/value of the call we find the difference between present value of the stock price and strike price.

N(d1) is the option delta gives you the responsiveness in the value of the option to a change in the value of the underlying asset.

N(d2) is the risk neutral probability of the option being in the money.

In effect to arrive at the value/price of a call option we are deducting the strike price of the option multiplied by the probability of the option being in the money from the present value of the stock price multiplied by option delta. In case of the put option, we are doing the opposite we are subtracting the present value of the stock price multiplied by option delta from the strike price of the option multiplied by the probability of the option being in the money.

d1 and d2 are the mathematical derivations using calculus that you can leave for Manjul Bhargava or Brian Greene !

Template to use Black Scholes Model

Given above is the link to a spread sheet template for using the Black Scholes model. You just have to input the variables in the yellow fields to arrive at the option price.

The template has been tried on some listed stock options on CBOE and the option prices are quite close to the actual bid ask quotes. Hope you find it useful!

(Source: Prof Damodaran Real Options)

Comments

Post a Comment