Black- Scholes Model for Non Math Users

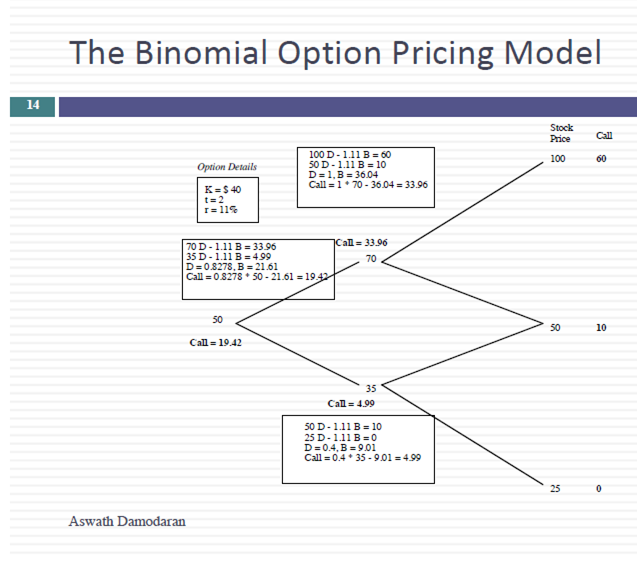

There are two kinds of people on this planet. Mathematicians who may constitute 0.001% (or even lesser than that!) of the total population and the other lesser mortals. So if you are one of those lesser mortals (like me!) and you want to use the Black Scholes model then, this article is for you. This article is based on Prof. Damodaran's real options pricing theory. To understand Black Scholes without delving too much into calculus, one needs to the understand two concepts - a) replication portfolio and b) arbitrage. To value or price an option we replicate the cash flows from the option by using other financial instruments as described below. Call = Borrowing + Buying D of the Underlying Asset Put = Selling Short D on Underlying Asset + Lending To replicate the cash flows on a call option without actually buying the option, we need to borrow some money (put in some personal equity) and buy D units of underlying asset. At the end of the time period if the stock price goes up you...